Last Updated on June 8, 2026

It is very important to have life insurance for yourself, especially if you have diabetes. You may think that in order to be eligible for diabetes life insurance, you have to undergo a medical exam, and have your medical records reviewed. This is not true.

Currently in the United States, there are nearly 31 million people with Type 2 Diabetes, 1.25 million people living with Type 1 Diabetes, and another 84 million have Pre-Diabetes.

It is very possible for people living with diabetes to find affordable diabetic life insurance coverage, and there are actually several different choices of coverage available to the Diabetes community. You may be eligible for non-medical exam life insurance for diabetics, and just not know it! Everyone’s Diabetes history is different, so please simply request a quote, and an agent can determine the various options available to you.

What Is Non-Medical Exam Life Insurance for Diabetics?

Non-medical exam life insurance, also known as no exam life insurance, is a type of policy that does not require blood tests, urine tests, or additional testing when applying for life insurance coverage.

The majority of traditional life insurance companies often require the applicant to have a medical exam, completed by an examiner, before qualifying for a life insurance plan.

This is because life insurance companies tend to prefer to ‘fully underwrite’ a person, who has Diabetes. They will want to review your lab results, in addition to the last 5 years worth of your medical and Diabetes records. All of this information would be used by an Underwriter, to make a formal offer of life insurance coverage. The rates will vary from person to person, and again are determined by a review of a person’s complete health profile.

This is because life insurance companies tend to prefer to ‘fully underwrite’ a person, who has Diabetes. They will want to review your lab results, in addition to the last 5 years worth of your medical and Diabetes records. All of this information would be used by an Underwriter, to make a formal offer of life insurance coverage. The rates will vary from person to person, and again are determined by a review of a person’s complete health profile.

Life insurance companies look at diabetes as a progressive disease. This means that the longer you have had it, the more susceptible you are to complications from the elevated blood sugar, and thus the more risky you are to insure. This is part of the reason why type 1 diabetics who were diagnosed early in life (usually before age 30) have a harder time getting insured than type 2 diabetics who were diagnosed after 30 and are able to better control their condition.

Good news! If you don’t want to wait weeks for an offer of coverage, or if you don’t want to go thru these hoops and hurdles, you can opt for a no medical exam life insurance policy for diabetics.

What is the Application Process Without an Exam?

The application process is pretty similar to traditional life insurance policies, minus the examination. Applications can be completed electronically, or if you prefer, you can print them out, and put pen to paper. You’ll provide the life insurance companies your pertinent information such as:

- Age of Diabetes Onset

- Current medications, if any, being prescribed to help control your diabetes.

- Any use of Diabetes technology such as a CGM?

- Most recent A1C reading.

- Any diabetic complications?

- How often do you test your blood sugar

- Any other medications currently taking outside of Diabetes medications?

- Any major health issues?

- Any use tobacco products within the last year?

- Approximate height and weight.

In addition to this information, insurance companies will also do a motor vehicle record review, a prescription drug background check, and a review of your MIB report. Certain companies may also review your medical records. Not all will, but some can require them. The information gathered, determines if you qualify, or not.

If not wanting companies ‘snooping’ thru your records, just let your agent know this up front. They can make recommendations based off your preferences. Non medical exam life insurance with Diabetes doesn’t have to be confusing. Simply contact us, have a brief conversation, and from there we can provide you with all the information you are seeking.

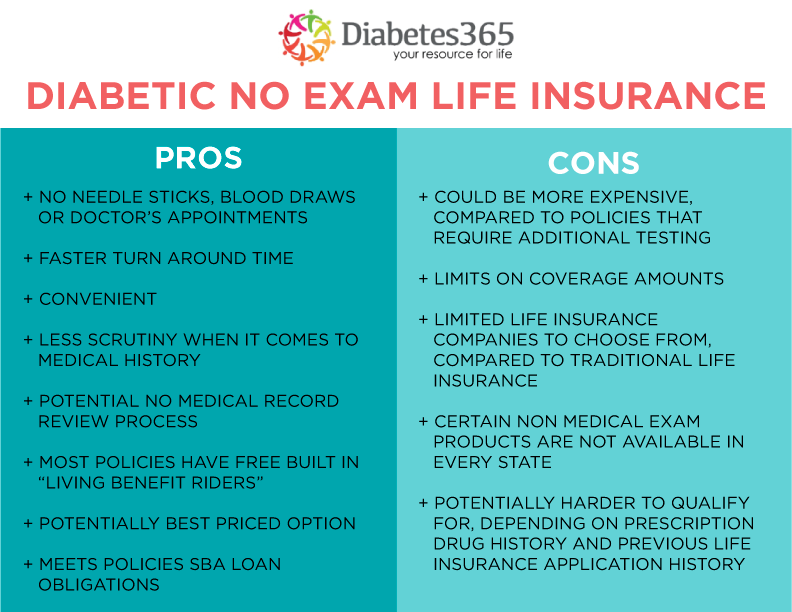

Pros & Cons of Non-Medical Exam Life Insurance

Pros:

- No needle sticks, blood draws or doctor’s appointments

- Faster decision (Some get approved in just a few minutes, but most get approved within 72 hours)

- Convenient

- Less scrutiny when it comes to your medical history

- Possibility of not having medical records reviewed.

- Most policies come with free built in “living benefit riders”

- Could be your BEST PRICED option

- Perfect for policies to meet SBA Loan obligations

Cons:

- Could be more expensive, compared to policies that require additional testing

- Limits on coverage amounts

- Not as many life insurance companies to choose from, compared to traditional life insurance

- Certain non medical exam products are not available in every state

- Could be tougher to qualify for, depending on your prescription drug history, and previous life insurance application history

Who Qualifies for Non-Medical Exam Diabetic Life Insurance?

Believe it or not, almost anyone with Diabetes, qualifies for some type of non-medical exam life insurance policy. However, people who typically purchase non-medical exam life insurance tend to fall under one of the following categories: People with “white coat” syndrome who want to escape the stress of a medical exam and the dread getting poked with a needle during a blood draw.

Or maybe you are a very busy person and cannot make any time to schedule an exam, People needing insurance in a hurry for a purpose, such as to collateralize a loan, meet a divorce obligation, and People who only require a smaller amount of life insurance (less than $500,000) are often prime candidates for a policy that does not require a medical exam

+ People with Type 1 Diabetes

If you have Type 1 diabetes or you are an insulin-dependent diabetic, diagnosed before the age of 30, you will typically face the largest challenges for qualifying for life insurance coverage. However, you would still have options for Term and Whole Life Insurance that wouldn’t require an examination. The number of options available to you is limited when compared to people diagnosed with diabetes later in life.

If you were diagnosed with Type 1 Diabetes before age 30, and are in need of a Term Life Insurance policy without a medical exam, more than likely companies will review your last three to five years worth of Diabetes records. If diagnosed at age 30 or later, then several companies would consider without an exam, or review of medical records.

If you were diagnosed with Type 1 Diabetes before age 30, and are in need of a Term Life Insurance policy without a medical exam, more than likely companies will review your last three to five years worth of Diabetes records. If diagnosed at age 30 or later, then several companies would consider without an exam, or review of medical records.

What if you are in need of a permanent form of life insurance? If your financial objectives fit this type of life insurance product, there would companies that would offer up to $100,000 in coverage, no matter the age of your Type 1 Diabetes. Different products, and companies would be determined by, the state you reside in.

To determine rates and eligibility, the various life insurance companies are going to simply ask if you questions about your Type 1 Diabetes history, use of Diabetes related technology, and other health questions. If you use an insulin pump, we’d simply ask a few follow up questions to this matter. Or maybe you have an artificial pancreas. If that’s the case, again, there would be additional questions that we would ask. The Diabetes technology world is constantly changing, and this is why you want to work with specialists such as Diabetes 365 !!!! WE will help you find the best life insurance company, based off your Diabetes profile!!!

+ People with Type 2 Diabetes

It is typically easier to qualify for life insurance for Type 2 diabetics. Some life insurance companies are much more lenient with applicants who are able to control their diabetes through diet and exercise and/or with an oral diabetes medication and Insulin. If having Type 2 Diabetes, that will open more doors, and you’ll have more options to choose from. In the life insurance world we currently live in, companies tend to favor people who have Type 2 Diabetes, compared to an individual with Type 1 Diabetes when applying for no medical exam life insurance policies. This means that your rates may be lower, depending on your Diabetes history.

If you do not require insulin to control your blood sugar, there are potential workarounds for getting a competitively priced policy approved with similar rates as person who applies using a medical exam policy. Type 2 diabetics with an A1C of 8.0 or lower will usually have an easier time finding the most affordable life insurance rates. If A1C is 10.0 or lower, you’ll still have options. It’s always a good idea to contact us, explain your situation, and let the Diabetes Life Insurance experts guide you thru your search of life insurance.

+ People with Prediabetes

Having Pre-Diabetes should not have any impact, on you qualifying for a no medical exam life insurance policy. Assuming that you are following Doctors orders, possibly exercising and watching your diet, the process should be a ‘breeze’.

You may qualify for Term Life Insurance policies up to $1 Million in coverage, where an approval is made in minutes or within 48 hours. Permanent insurance could also be obtained in a matter of minutes or days.

As long as there’s no red flags in your prescription history, or any other significant health issues, your rates would be the same as a person who isn’t considered Pre-Diabetic. For the majority of non medical exam life insurance providers, Pre-Diabetes isn’t a concern

+ People with History of Gestational Diabetes

Gestational Diabetes is more common than most people think. American Diabetes Association even claims that nearly 9.2% of women who are pregnant, can be diagnosed with Gestational Diabetes.

Luckily, history of Gestational Diabetes has little impact on your non medical exam life insurance with Diabetes. Companies are going to be mainly concerned with your current height, weight, and other lifestyle choices. The main thing we recommend is to be compliant with your Doctor’s instructions. Meaning if they encourage your to watch your diet, exercise, refrain from alcohol, then please listen to your medical professional.

People with history of Gestational Diabetes should have no issues qualifying for both Term and Permanent insurance products. There would be a plethora of options for you to choose from. Simply speak with one of our licensed agents, and let them help find you the best type of policy given your financial needs.

Common Types of Non-Medical Exam Life Insurance for Diabetics

The most common life insurance options that do not require a medical exam include:

No Medical Exam Term Life Insurance

If you’re between the ages of 21 and 70 you can purchase a policy without an exam for $25,000 to $500,000 in death benefits. The rates for term life insurance for diabetics are fixed and are available in 10, 15, 20, and 30 year terms.

There is no obligation to keep the term life insurance policy for the entire duration. If you no longer wish to have the life insurance policy, you can simply cancel it at any time. By doing so, the life insurance policy will no longer be in force.

Many term policies come with the discussed ‘living benefit riders’ at no extra fee to you. If diagnosed with a Chronic, Critical, or Terminal Illness, you could accelerate part of the death benefit, while living, and use the life insurance benefit as you see fit.

Guaranteed Universal Life Insurance (GUL)

Guaranteed Universal life insurance policies offer a fixed death benefit of up to $500,000 with a fixed monthly cost guaranteed not to change as you get older. GUL’s are available for applicants between the ages of 21 and 75, and also known as term-to-Age 100 policies because these policies offer rates and coverage that is guaranteed until age 80, 85, 90, 95, or 100 or later. As the insured, you can really ‘dial’ in the length of a policy you want, to match your financial needs. These policies are a great alternative to expensive non-guaranteed universal life insurance policies because they are provide GUARANTEED premiums.

These policies may be ideal for a person who simply wants permanent life insurance coverage, and isn’t worried about the ‘cash value’ of a policy. Guaranteed Universal LIfe policies are considerably less expensive, compared to Whole Life Insurance policies.

Level Death Benefit Whole Life

These Whole Life Insurance policies tend to be expensive, but if your health is average or better, they are very easy to qualify for. As you are probably aware, Whole Life insurance is a form of permanent insurance, with guaranteed level rates.

In addition to providing life insurance coverage, Whole Life Insurance policies accrue cash value over time. The cash value could be accessed thru a ‘policy loan’, or if you surrendered the policy.

In addition to providing life insurance coverage, Whole Life Insurance policies accrue cash value over time. The cash value could be accessed thru a ‘policy loan’, or if you surrendered the policy.

The policy covers a person’s entire life. At the time of death, the policy will pay the death benefit to the beneficiary, in a lump sum payment.

People with Type 1 and Type 2 Diabetes would have several options for these non medical policies. You could purchase a policy without an exam from $5000 to $100,000 in coverage.

The older you become, the lower amount of coverage may be offered by the various companies. Companies will begin offering lower limits of Whole Life Insurance as you enter your 60’s, 70’s, and 80’s.

Some people take out smaller amounts of non medical exam Whole Life Insurance to cover burial costs, and final expenses. Policies like these are easily obtainable, and very affordable for Diabetics.

Guaranteed Issue Life Insurance for Diabetics

Guaranteed issue policies offer up to $25,000 in death benefits for those who are between ages 40 and 85 and have serious health issues. These policies are the ones that you normally see advertised on TV by celebrities or AARP and they tend to be expensive for the amount of coverage you receive because “no health questions are asked.”

Since a person cannot be turned down for coverage, the Whole LIfe Insurance policy will have a TWO year waiting period on paying out the full death benefit of the policy. If a person passes away of natural causes in first TWO years, all premiums paid into policy plus 10% is refunded to beneficiary. If death occurs at any time after the first two years, then full amount of policy is paid to beneficiary.

Here are some sample rates for Guaranteed Issue Life Insurance for Diabetics

Male Monthly Rates

| Age | $5,000 | $10,000 | $15,000 | $20,000 | $25,000 |

|---|---|---|---|---|---|

| 50 | $19.66 | $38.41 | $57.15 | $75.90 | $94.65 |

| 55 | $23.55 | $46.11 | $68.70 | $91.31 | $113.90 |

| 60 | $28.78 | $56.65 | $84.52 | $112.38 | $140.25 |

| 65 | $34.60 | $68.29 | $101.98 | $135.67 | $169.36 |

| 70 | $44.41 | $87.91 | $131.41 | $174.90 | $218.40 |

| 75 | $62.79 | $124.67 | $186.54 | $248.42 | $310.29 |

| 80 | $110.92 | $220.92 | $330.92 | $440.92 | $550.92 |

Female Monthly Rates

| Age | $5,000 | $10,000 | $15,000 | $20,000 | $25,000 |

|---|---|---|---|---|---|

| 50 | $14.53 | $28.14 | $41.75 | $55.37 | $68.98 |

| 55 | $18.38 | $35.84 | $53.30 | $70.77 | $88.23 |

| 60 | $23.70 | $46.48 | $69.25 | $92.03 | $114.81 |

| 65 | $28.19 | $55.46 | $82.73 | $110.00 | $137.27 |

| 70 | $34.83 | $68.75 | $102.67 | $136.58 | $170.50 |

| 75 | $45.60 | $90.29 | $134.98 | $179.67 | $224.36 |

| 80 | $76.54 | $152.17 | $227.79 | $303.42 | $379.04 |

Graded Death Benefit Whole Life Insurance

Similar to a Guaranteed Issue Life product, these policies won’t pay out the full death benefit until policy is TWO years or older. However, if you can answer NO to a few health questions, some Life Insurance companies will offer policies that pay 40% of Death Benefit in year 1 of policy, and 70% of Death benefit of Policy in Year 2.

Policies like these may be less expensive compared to Guarantee Issue Whole Life Insurance policies, and would more of a death benefit in the first Two years of a policy.

To determine what plans are ideal for your situation, please simply contact us. We’d love to help make recommendations that are suitable given your health profile.

What Types of Life Insurance Riders are Available?

Great news for people living with the various Types of Diabetes! Your policies can come with the same type of ‘riders’ that people without Diabetes can obtain. We’re going to outline a few of the most popular riders that our clients choose.

- Return of Premium Rider: With this ‘rider’, when your term life insurance policy is up, and assuming you are still alive, you receive all of the premiums you paid into policy back. This is paid lump sum, and is tax free.

- Waiver of Premium Rider: Waiver of premium rider is often times referred to as waiver of premium for disability. With this rider, if you became sick, or injured and could no longer work, the rider would go into effect. The rider would cover your policy, as no more premiums would be due from you. One in five americans live with a Disability, so a rider like this may be a good idea to consider.

- Accelerated Living Benefit Riders: In our eyes, these are some of the most important riders, or benefits you can have with a life insurance policy. Three main type of Living Benefit Riders are available, and most policies include all three:

Terminal Illness– This benefit would allow the owner of policy to receive a portion of the death benefit, if the insured was diagnosed with a Terminal Illness. Owner would simply provide written evidence from a Doctor supporting that the insured has an illness that is expected to result in death within twelve months.

Chronic Illness– This benefit allow the owner of policy to receive a portion of the death benefit if the insured is diagnosed with a Chronic Illness. Again, you’d provide written evidence from a medical professional, stating the following: (1) Not being able to perform at least two activities of daily living for at least 90 days, as defined in the rider, or (2) Requiring substantial supervision due to severe cognitive impairment for at least 90 days, as defined in the rider.

Critical Illness– With this benefit, the owner can elect to receive payment of a portion of the death benefit if the insured is diagnosed with a Critical Illness. The owner of policy provides evidence for a licensed Physician, confirming the qualifying event. Some qualifying events are Heart Attacks, Strokes, Cancer, Renal Failure, or an Organ transplant.

Obtaining Life Insurance for Diabetics is always an important decision for you and your family. But discussing specific ‘riders’ are equally as important. It doesn’t have to be confusing or complicated. Simply visit with one of our agents, who can help you with these life altering decisions.

To get a free quote for non-medical exam life insurance simply fill out the form on the right hand side of the screen. Or better yet, give us a call. We only work with the Diabetes community, so we are trained compared to other agencies that work with all types of health conditions. These groups are ones to avoid.

We provide a first class customer service experience to all of our clients. Make the phone call today!