Last Updated on July 23, 2026

Life insurance is as important a risk management tool as it sounds. It gives you or your family protection in case of emergency so that you will not be left destitute and out on the streets in the event of the death of the primary income earner for the household. Thus, it also gives you peace of mind, which should be an inherent right afforded to all.

Having Pre-Diabetes, Gestational Diabetes, Type 1 Diabetes or even Type 2 Diabetes can make it a little more challenging finding life insurance coverage. However, companies like Diabetes 365 were created to specifically help diabetics find affordable coverage.

The paradox is that diabetic life insurance cannot be afforded by all. Not true at all. Rates are probably lower than you think!!!! Life insurance rates for Type 1 Diabetics, and Type 2 Diabetics are at an all time low. Of those who can afford it, some—potentially millions of them—may not qualify for life insurance for with Diabetes. Why?

Some of those millions have a history of drug addiction. How will companies view your health profile with a drug usage history, in addition to Diabetes? Let’s dive into what Diabetes life insurance carriers will be looking for.

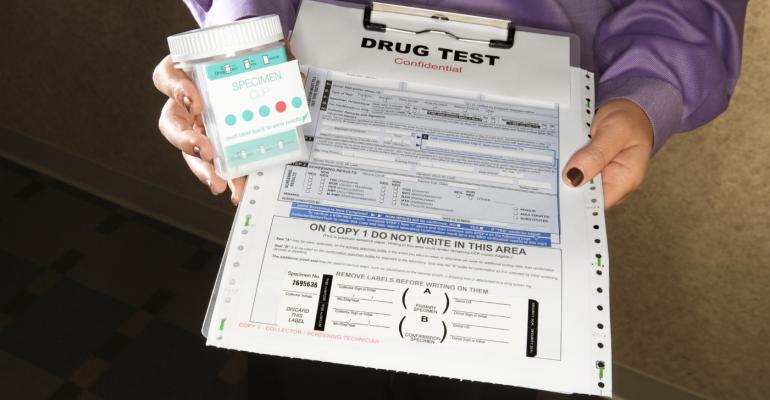

Drug Usage and Life Insurance

While not all life insurance companies require drug tests for those applying for a policy, a good number of them will test blood work and urine samples for alcohol and illegal and prescription drugs prior to approving a life insurance policy. If you are the type of person who doesn’t want to complete a blood or urine test, there may be some non medical exam life insurance policies for diabetics available to you.

One of the things they test your urine and blood for is for the usage of Drugs. In additions, they test your A1C, Glucose levels, and usage of Tobacco products.

Tests that will be gathered from your bodily fluids:

- Cholesterol

- Triglycerides

- Creatinine

- Urine Creatinine

- Microalbumin

- HIV

These lab results, in addition to a review of medical records will determine what life insurance rates can be offered, if any.

If you have been using illegal drugs, such as Heroin, Cocaine, or Meth, you will declined immediately. Most companies will want you to refrain from using these drugs fro up to a year, while other diabetic life insurance companies may want you to be drug free for six months.

What if I’ve Quit Using Drugs?

In addition to your diabetes history, companies will want to know if you are a previous drug user.

They will ask the following questions about your drug use:

- How long have you quit? (most companies want you drug free for 12 months or longer)

- How long were you using drugs?

- What type of drugs were you using? (different kinds are deemed more harmful: cocaine & heroin > marijuana)

- Were you ever hospitalized from Drug Use?

- Did you ever receive treatment for Drug use?

- Are you currently employed? Married? Companies will want to see that you are living a “stable lifestyle”

Never Lie on Your Life Insurance Application

It’s true that it is actually possible to flush out illegal substances from your body in such a way that the drugs will not show up during tests. However, insurance companies will eventually find you out. Especially if you apply for a policy that requires a review of your medical records, and there’s notes in there of drug use.

Don’t forget that this industry has been around for years and whatever trick you have up your sleeve, there is a high probability that somebody else has already tried it in the past — and failed.

Plus, Diabetes life insurance companies are not magnanimous entities. They are a business. Thus, a huge part of their operational efforts and personnel are dedicated to ferreting out the truth. The easiest way to do this is to prove that you committed fraud by lying on your application. The contract then becomes moot no matter how much you paid and how many years you’ve been paying.

If you want to get approved, please be honest. When working with an independent agent from Diabetes 365, we will already do our best to ‘shop’ your case out to multiple companies. But we will need you to provide honest details to your Diabetes history, and drug use history.

Is it Legal for Insurance Companies to Drug Test?

Life insurance companies are within their legal rights to conduct a drug test before you can purchase a life insurance policy from them. It’s the same way when you apply for a job and the employer can insist you take the drug test first. Depending on the amount of coverage you are seeking, companies may require the blood and urine test. Testing your labs for drug use is one part of the equation for a life insurance company.

Life insurance companies reason that the results of these tests will allow them to compute your premiums or how much you have to pay them on a regular basis.

Life insurers that require drug tests will usually conduct a full battery of them and search your system for amphetamine/methamphetamine, barbiturates, benzodiazepines, cocaine, methadone and other opiates, and phencyclidine (PCP).

While many life insurance companies will automatically decline your application because of a positive drug test, the same isn’t necessarily true for a past history of drug abuse.

If you have already been to an effective substance abuse treatment program and can prove that you are truly recovered and have become a fully functional and productive member of society—one who has a job and maybe even formalized civic responsibilities—you might have a shot.

The Magic Number

In part, it depends on the number of years that you have been drug- or alcohol-free. The magic numbers are usually 1 and 3 years. Those who have been drug-free for three or more years can apply for diabetes life insurance, and not accessed any extra premiums to the policy. In the meantime, those who have been drug-free for more than 10 years very well may be eligible for standard to preferred rates, depending on Diabetes and health issues.

Perhaps not so surprisingly, the situation is worse for smokers. Nicotine is possibly the most addictive drug in the world, and tobacco smokers have worse health outcomes overall than non-smokers. If you test positive for nicotine or marijuana, you can expect higher insurance premiums and more limited insurance coverage.

Nicotine is the main addictive substance in cigarettes and other forms of tobacco. Nicotine is a drug that affects many parts of your body, including your brain. Over time, your body and brain get used to having nicotine in them. About 80–90% of people who smoke regularly are addicted to nicotine.

Life insurance companies often have separate rates for their “preferred” or healthy clients—also called non-smoker rates—and separate rates for the smokers. Preferred clients have lower premiums, the amount of money that you agree to pay for a life insurance policy at one time or on a regular basis.

Many believe that marijuana users should not be lumped in with other applicants who have used other illicit drugs. Thirty of the 50 states have legalized the use of medical marijuana, including Oklahoma which voted for legalization last June. Recreational use also has been legalized in nine states plus in Washington, DC.

Many believe that marijuana users should not be lumped in with other applicants who have used other illicit drugs. Thirty of the 50 states have legalized the use of medical marijuana, including Oklahoma which voted for legalization last June. Recreational use also has been legalized in nine states plus in Washington, DC.

However, life insurance companies don’t seem to care about this distinction and —at least so long as marijuana remains illegal under federal law—they don’t have to.

Some life insurance companies may put marijuana users in a separate, higher-premium category from smokers. Rates for smokers are already thrice the amount for the non-smokers or “preferred” policyholders.

High-Risks Applicants

Aside from illicit drugs, life insurance companies may also conduct tests to look for certain prescription drugs that have a high potential for abuse and addiction.

After the US government admitted that the country is in the midst of an opioid epidemic, painkillers and muscle relaxers have become controversial, particularly oxycodone, hydrocodone, fentanyl, and benzodiazepines.

Life insurers also look for the presence of medications for:

+ Diabetes – You might think it is unfair to discriminate against diabetics, but to the mind of life insurers, they are considered to be at a higher risk, health-wise, compared to non-diabetics.

+ HIV – Many life insurance providers would prefer HIV clients to instead purchase accident insurance or limit their coverage to a certain amount. Some minds are changing about them, too, though not very quickly.

+ Mental Health – Insurers also look for prescribed medications for such mental health problems as ADHD, anxiety/depression, bipolar disorder, dementia, and schizophrenia.

+ Parkinson’s Disease – Insurers keep an eye out for medications that treat Parkinson’s, too. The progressive disease of the nervous system can lead to tics and tremors, a rigidity of the muscles, and an inability to control one’s own movements.

Companies permit the purchase of a life insurance policy by prescription drug users if the applicants can still function in society despite the underlying diseases, conditions, and prescribed drug use.

Companies permit the purchase of a life insurance policy by prescription drug users if the applicants can still function in society despite the underlying diseases, conditions, and prescribed drug use.

Employment and hospitalization records will be checked. If these show stability, then the application should go smoothly and they can purchase life insurance at the “standard” rates with maximum coverage, as long as the Diabetes is well controlled and no other health issues..

You still can purchase life insurance for you or your family, even if you are a recovering drug user. Don’t hesitate and don’t get frustrated. There are hundreds of life insurance companies, but not ALL of them will approve people with Diabetes, and who have history of drug use.

Work with a Diabetes Life Insurance Specialist, such as ourselves. Everyday we speak to people with Diabetes, and other health issues. Let us help you find the best diabetes life insurance policy out there for you!!!

We work with DOZENS of life insurance companies who underwrite the diabetes community fairly. And companies that are lenient when it comes to drug abuse history.

You will probably have several types of options, when it comes to your policy choices. Diabetic term life insurance or even whole life insurance for diabetics policies that will protect you and your family.

Contact us today, to begin getting your no obligation life insurance quote.