Matt Schmidt is a nationally licensed diabetes insurance expert. Over this time frame he's helped out over 10,000 clients secure life insurance coverage with Diabetes. He's frequently authors content to Forbes, Entrepreneur, The Simple Dollar, GoBanking Rates, MSN, Insurancenews.net, and Yahoo Finance and many more.

Matt Schmidt is also the Co-Founder of Diabetes Life Solutions and Licensed Insurance agent. He’s been working with the Diabetes community for over 18 years to find consumers the best life insurance policies. Since 2011, he has been a qualified non-member of MDRT, the most prestigious life insurance trade organization in the USA

Fact Checked By

Chris Stocker

Chris Stocker

Chris Stocker is a financial services professional and licensed insurance agent. He's also Owner and author of The Life of a Diabetic as well as Type 1 Detour. He's been writing about Diabetes related topics for over 10 years, and has been featured in HealthLine, Diatribe, Diabetes Advocates and JDRF.. He's been writing about Diabetes related topics for over 10 years, and has been featured in HealthLine, Diatribe, Diabetes Advocates and JDRF.

Diabetes 365 follows very strict guidelines for accuracy and integrity on all content. To learn about Diabetes 365 commitment to transparency and integrity, read our Editorial Disclosure

Last Updated on July 4, 2026

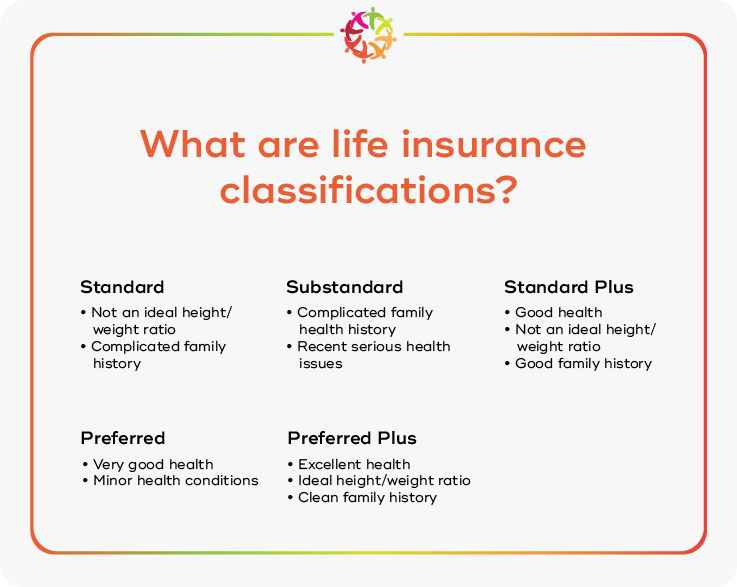

Are you a person with diabetes searching for life insurance? Learn why securing a diabetes life insurance policy can be more affordable than you think. Life insurance for diabetics does not have to be difficult. Diabetes 365 is here to provide the most accurate life insurance information possible to those living with diabetes. Do not let other websites or agents ‘trick’ you by allowing them to quote you Preferred or Preferred Plus rates. Less than 1% of the Diabetes population will qualify for underwriting classifications like these.

Diabetes 365 was created to help people in the Diabetes community obtain the valuable life insurance coverage their family needs. For whatever reasons, there is all types of misinformation on the internet from sites like Investopedia and Policy Genius. IF you’re wanting to review real and accurate Diabetes life insurance information, you’ve come to the right website.

People who live with any type of Diabetes should not feel like they cannot obtain life insurance. The truth is, people with Pre-Diabetes, Gestational Diabetes, Type 1 and Type 2 Diabetes can qualify for affordable life insurance coverage. Many individuals within the Diabetes community feel like they cannot qualify for a policy. This is simply not true. Fill out a quote request, or contact us to let an agent provide you with all the information you are seeking.

Like many things in this world, Covid 19 has impacted the life insurance industry tremendously. Life insurance companies have made many changes to their underwriting guidelines over the last 12 months. People with Diabetes have really been affected due to these changes in underwriting. As an example, some life insurance carriers are NO LONGER offering coverage to a person with Diabetes. Or for many with Type 1 Diabetes, companies may not currently accept your health profile due to changes in the marketplace. Some restrictions are slowly being lifted, but companies are monitoring the ever changing situation very closely.

Our mission at Diabetes 365 is to help people with Diabetes, secure the best life insurance policy possible. We understand the importance of life insurance with diabetes, and the need to protect your family from a financial struggle in the event of premature death. At Diabetes 365 you’ll only receive honest life insurance information from our agents. Since we are a part of the Diabetes community, we only operate with the highest level of ethics.

Not only do we provide consumers with real and accurate life insurance rates, but we’ll also help guide an applicant through the application process. This includes assisting you with completing the initial application, scheduling the paramedical examination, and if needed ordering necessary medical records from your medical professionals. We stay in touch with you every step of the way, and provide you with updates every few days.

Perhaps you’ve been declined life insurance due to diabetes, and are starting to feel like you don’t qualify for coverage. Well don’t ever feel that way. Simply fill out our online quote request, and let an agent who specializes in life insurance with Diabetes assist you.

Having Diabetes does make it more difficult to find affordable life insurance for diabetics, but it’s not impossible. Life insurance companies have begun to treat the diabetes community a little more fairly, in terms of underwriting. By doing so, diabetes life insurance rates are at an all time low. Not to mention, there’s never been more choices for people with diabetes, when it comes to diabetic life insurance companies to choose from.

Sadly, when it comes to finding accurate information for diabetes and life insurance, it can be an uphill battle. Lots of websites on the internet tend to provide fake and misleading information to the diabetes community. As a hint, if a website or agent quotes you Standard Plus, Preferred, or even Preferred Plus rates, there’s a really good chance they are providing false information.

Why? Less than 5% of applicants with Diabetes qualify for Standard Plus rates. And less than 1% of applicants who have a history of Diabetes receive Preferred or Preferred Plus offers. If you see a website advertising these low ball life insurance quotes, run as fast as possible!

According to the American Diabetes Association, over 34 million people in the United States alone have Diabetes. Another 84 million have pre-diabetes. Life insurance companies have changed over time, and now view people with diabetes as a more acceptable ‘risk’. In our humble opinion, we think people with diabetes are extremely healthy. Most people with diabetes are exercising, testing their blood sugar levels, and watching everything they eat.

Since Diabetes365 ONLY works with the diabetes community to help them secure life insurance, we have access to companies that may offer pricing up to 20% cheaper than the retail pricing.

How? By showing life insurance companies that your diabetes is under control, and by using technology to allow them to see your physical activity. Wearable devices like Apple Watch, or FitBit are great tools that many people with diabetes use. If wanting to share this information with an insurance company, it may lead to considerable discounts on life insurance.

One of the best ways to get declined for coverage is by working with the wrong agent, or agency. Many agents are not properly trained to work with people who have a form of diabetes. Because of this, thousands of diabetics are declined for coverage each year. An agent who isn’t properly trained may have you apply to a company who would decline you automatically, due to your specific diabetes history. Or they could have you apply to a life insurance carrier, who charges higher premiums to people who have diabetes. This may lead to paying thousands of dollars more for life insurance, over the lifetime of a policy.

Working with an agency such as Diabetes365 may result in thousands of dollars in savings, on your life insurance premiums over time. We only work with the diabetes community, and understand which companies may be the most competitive, given your complete health history. Let us show you how easy obtaining diabetes life insurance can be!!! Don’t fall victim to other agents who lie, and provide fake quotes. Nothing is more frustrating than applying, and having the final price be 100% higher.

When working with us, you’ll only receive REAL and ACCURATE quotes. If wanting fake information, we can send you to some other websites that we know, who mislead the diabetes community.

To receive information, simply fill out the quote request form, to the right of this page. We will then use the diabetes information, and health history you provide us, to find the best possible policy for you and your family. Diabetes365 will do all of the hard work on your behalf! We’re your personal life insurance shoppers!!!

Source: Project Blue November

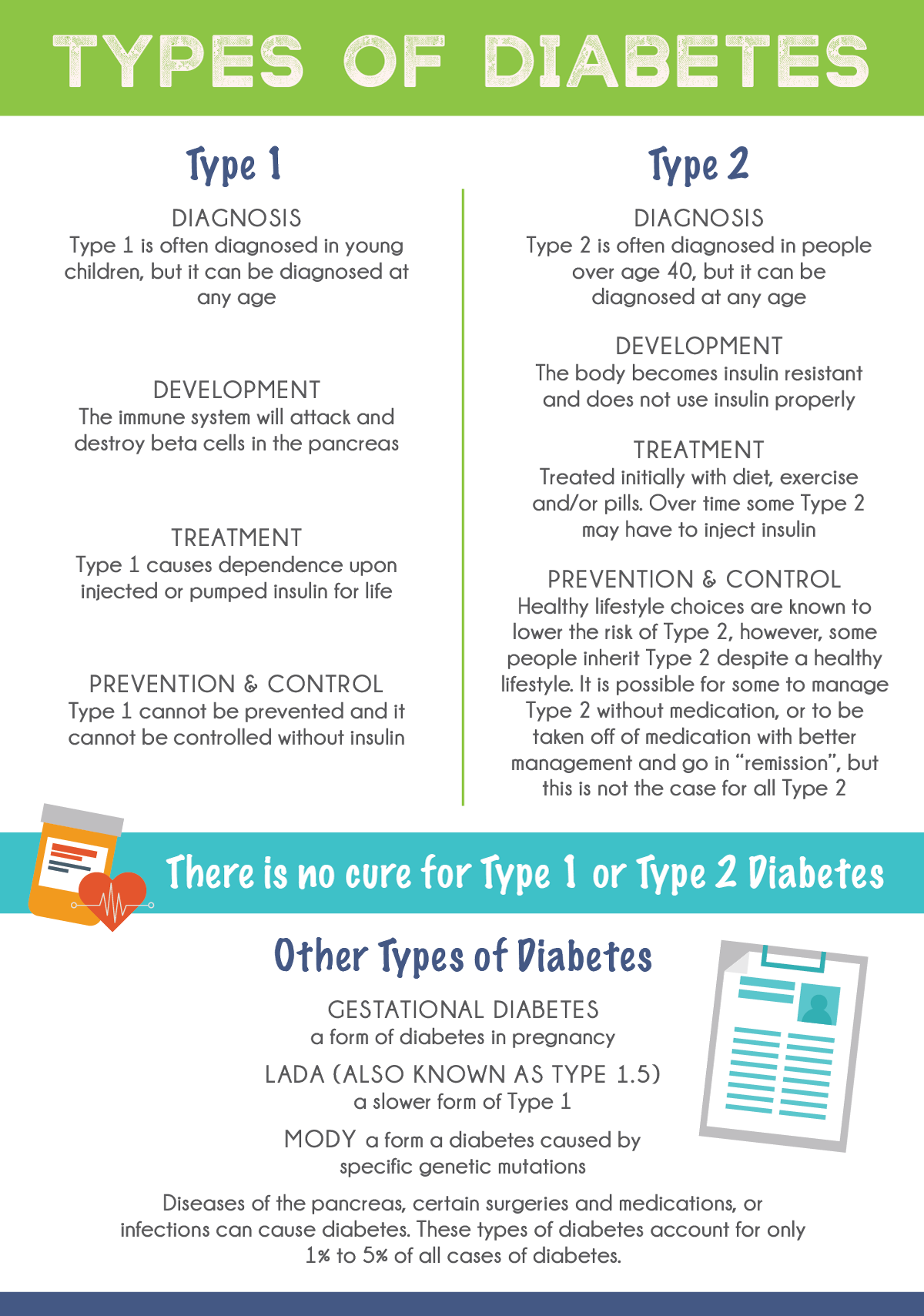

What Exactly is Diabetes

Type 1 Diabetes

According to Healthline, Type 1 diabetes is a chronic disease. In type 1 diabetes cells in the pancreas that make insulin are destroyed, and the body is unable to make insulin.

Insulin is a hormone that helps your body’s cells use a natural sugar called glucose for energy. Your body obtains glucose from the food you eat. Insulin allows the glucose to pass from your blood into your body’s cells. Your liver and muscle tissues store extra glucose, also called blood sugar. It’s released when you need extra energy, such as between meals, when you exercise, or when you sleep.

In diabetes mellitus type 1 the body is unable to process glucose due to a lack of insulin. This causes elevated blood sugar levels and can cause both short-term and long-term problems. Now the good news, It’s quite possible to find affordable life insurance policies, even if you live with type 1 diabetes. Life insurance rates may even be less expensive than you think.

Finding life insurance with type 1 diabetes will be a challenge. Not all life insurance carriers will offer coverage to people with type 1 diabetes. Living in the current Covid 19 environment is also challenging. Less companies are offering coverage at the current moment. Simply stated, you’ll have fewer choices than in recent years in terms of life insurance companies to choose from. Life insurance for type 1 diabetics will most likely be more expensive, compared to people with other types of diabetes. Life insurance companies will view you as a higher risk, and most likely your premiums will be higher.

Why? People with type 1 diabetes generally are diagnosed with diabetes at a younger age, and are at a higher risk of developing diabetes complications. This isn’t always the case as a person’s complete health profile will be reviewed, to determine final rates. If you are diagnosed with Type 1 Diabetes in your 20’s, 30’s, 40’s or even your 50’s, rates will be more favorable.

Please understand that very few people with type 1 diabetes will receive an underwriting classification Standard or better. Most likely, your health profile will be substandard or table rated. Generally the higher the table rating, the higher your life insurance premiums will be. Routinely we are seeing well controlled diabetics with Type 1 receive Table C to Table E offers. Sometimes even better.

Below are some of the main criteria that Underwriters will use, to determine what rates are available:

Age first diagnosed with Type 1 Diabetes

Any diabetes complications?

Level of control of your Type 1 Diabetes and A1C history

Since every life insurance company has different underwriting guidelines, carriers will view your diabetes profile differently. One may decline you all together, while another would approve you with minimal increase in premiums. The better your A1C and overall health, the better your life insurance rates will be. Sadly, 99% of the time, life insurance companies will not offer Standard, or better ratings, to the type 1 diabetes community.

The reality is, having type 1 diabetes will lead to higher life insurance premiums. There’s really no way around it. The extra premiums that companies will charge are referred to as ‘table ratings’. Table ratings are determined by underwriters on a case by case basis. However, you’ll be able to possibly offset some of these extra premiums, by showing companies that you live a healthy lifestyle. Companies will apply ‘healthy’ lifestyle credits to your profile, lowering the cost of life insurance.

Don’t do the ‘guesswork’ yourself. Let us go to work on your behalf, and help secure the best Type 1 Diabetes life insurance rates possible! Just fill out the quote request, and let our agents go to work for you. We’ll simply recommend specific life insurance companies based on your health profile and Type 1 Diabetes history.

Sample $100,000 Type 1 Diabetes Term Life Insurance quotes

$100,000 Term Life Insurance – Table Rated

Male Non Tobacco User

10 Year Term

15 Year Term

20 Year Term

40 Year Old Male Non Tobacco User

$22 to $41 monthly

$24 to $45 monthly

$30 to $50 monthly

50 Year Old Male Non Tobacco User

$40 to $57 monthly

$48 to $65 monthly

$62 to $80 monthly

40 Year Old Female Non Tobacco User

$18 to $32 monthly

$21 to $35 monthly

$25 to $40 monthly

50 Year Old Female Non Tobacco User

$32 to $52 monthly

$39 to $60 monthly

$47 to $70 monthly

Sample $250,000 Type 1 Diabetes Term Life Insurance quotes

$250,000 Term Life Insurance – Table Rated

10 Year Term

15 Year Term

20 Year Term

40 Year Old Male Non Tobacco User

$40 to $65 monthly

$48 to $72 monthly

$59 to $77 monthly

50 Year Old Male Non Tobacco User

$85 to $110 monthly

$105 to $130 monthly

$136 to $174 monthly

40 Year Old Female Non Tobacco User

$31 to $50 monthly

$40 to $58 monthly

$50 to $70 monthly

50 Year Old Female Non Tobacco User

$61 to $80 monthly

$80 to $95 monthly

$100 to $125 monthly

Type 2 Diabetes

Can you get life insurance with Type 2 Diabetes? Most likely yes. Life insurance for Type 2 Diabetics tends to be less expensive than most think. Generally, an individual will have several life insurance companies to choose from. However this is determined on a case by case basis. Let’s look into some statistics of Type 2 Diabetes.

According to EverydayHealth, Type 2 diabetes, a form of diabetes mellitus, is likely one of the better-known chronic diseases in the world — and that’s no surprise. Data from the Centers for Disease Control and Prevention suggest in the United States alone, 30.3 million people, or 9.4 percent of the U.S. population, has diabetes, and the majority of these people have type 2.

Among those people with diabetes, 7.2 million don’t even know they have it, and now, more and more children and adolescents are being diagnosed with prediabetes and type 2 diabetes.

Whether you’ve been diagnosed with type 2 diabetes or have a family history of the disease, this condition can be scary. And with the required diet and lifestyle changes, as well as an increased risk for complications like amputations and heart disease, we don’t blame you for fearing it.

But living with type 2 diabetes doesn’t have to be devastating. In fact, when you know the facts about the disease, like how insulin resistance develops and how to mitigate it, how to spot the signs of diabetes, and what to eat if you receive a diagnosis, you can get the prompt treatment and diet resources you need to thrive.

Good news for the type 2 diabetes community. Life insurance for type 2 diabetics tends to be less expensive, compared to type 1 diabetics. People with type 2 diabetes will have more companies to choose from, and will have a plethora of no medical exam policies available to them.

Life insurance companies tend to view people with type 2 diabetes as ‘average’ risks, and most of the time, the applicant will receive an insurance rating similar to a person without diabetes at all. Carriers have evolved their underwriting guidelines, and will now offer Standard, and even Preferred ratings to applicants, if they qualify medically.

Truth be told, life insurance for type 2 diabetics has never been more affordable and easily obtained. There’s a plethora of options available. Just reach out to us and let us explore all your life insurance options!

We’ll help you identify the companies that are the most competitive based on your complete health profile.

Certain individuals with type 2 diabetes may qualify for Standard, Standard Plus, or Preferred life insurance ratings. These are the very same ratings that people without Diabetes qualify for. Everyone’s health profile is different, so please contact us or complete a quote request to determine what rates you may qualify for.

Many individuals with Type 2 Diabetes will also be able to qualify for life insurance policies that offer ‘living benefit’ riders. Having a policy that provides Chronic, Critical, and Terminal illness riders at NO EXTRA cost to you could be extremely valuable to you and your family in the future. Here’s a brief description of these riders from QuickQuote.com:

What is a chronic illness accelerated death benefits rider?

According to the Centers for Disease Control and Prevention, chronic diseases such as heart disease, stroke, and cancer are among the costliest of all health problems in the United States.

If you were to become chronically ill during the term of the policy, the company would advance up to 90% of the policy’s coverage amount ($500,000 maximum) to help you pay for treatment or to replace lost income.

To qualify for this benefit, a licensed health care practitioner has to verify that you’re unable to perform two out of the six activities of daily living (bathing, continence, dressing, eating, toileting, and transferring).

What is a critical illness accelerated death benefits rider?

If you were to suffer a critical health condition such as lung cancer, heart attack, stroke, or paralysis, you could be eligible to receive accelerated death benefits from your policy.

Once again, the company will advance up to 90% of the policy’s face amount ($500,000 maximum) if a licensed physician determines that you’re critically ill.

Can you get life insurance if you have a terminal illness?

Are accelerated death benefits with a terminal illness out of the question? Learn about terminal illness accelerated death benefits riders.

The terminal illness benefit is for more serious conditions where a licensed physician has diagnosed you have less than 12 months to live.

This policy will advance up to 100% of the policy’s face amount, with a maximum of $500,000.

Here are some sample rates on life insurance for people with Type 2 Diabetes:

$100,000 Term Life Insurance – Standard Rated

10 Year Term

15 Year Term

20 Year Term

40 Year Old Male Non Tobacco User

$12 to $25 monthly

$15 to $28 monthly

$17 to $35 monthly

50 Year Old Male Non Tobacco User

$23 to $35 monthly

$26 to $43 monthly

$32 to $50 monthly

40 Year Old Female Non Tobacco User

$11 to $23 monthly

$14 to $30 monthly

$16 to $32 monthly

50 Year Old Female Non Tobacco User

$20 to $35 monthly

$23 to $40 monthly

$28 to $45 monthly

$250,000 Term Life Insurance – Standard Rated

10 Year Term

15 Year Term

20 Year Term

40 Year Old Male Non Tobacco User

$21 to $37 monthly

$26 to $43 monthly

$32 to $50 monthly

50 Year Old Male Non Tobacco User

$47 to $65 monthly

$59 to $80 monthly

$74 to $95 monthly

40 Year Old Female Non Tobacco User

$20 to $35 monthly

$23 to $40 monthly

$26 to $45 monthly

50 Year Old Female Non Tobacco User

$36 to $52 monthly

$45 to $60 monthly

$57 to $73 monthly

Gestational Diabetes

According to the Mayo Clinic, Gestational diabetes develops during pregnancy (gestation). Like other types of diabetes, gestational diabetes affects how your cells use sugar (glucose). Gestational diabetes causes high blood sugar that can affect your pregnancy and your baby’s health. Life insurance for Gestational Diabetics is easily obtained, and oftentimes there are NO extra pemiums accessed to a persons profile.

Any pregnancy complication is concerning, but there’s good news. Expectant women can help control gestational diabetes by eating healthy foods, exercising and, if necessary, taking medication. Controlling your blood sugar can prevent a difficult birth and keep you and your baby healthy.

In gestational diabetes, blood sugar usually returns to normal soon after delivery. But if you’ve had gestational diabetes, you’re at risk for type 2 diabetes. You’ll continue working with your health care team to monitor and manage your blood sugar.

If you have a history of gestational diabetes, don’t think that you can’t qualify for life insurance. Life insurance with gestational diabetes is easy to obtain, and oftentimes will have little impact on your rates. Some applicants will have an easy time qualifying for Standard to Preferred life insurance rates. These are the very rates people without Diabetes tend to qualify for.

Life insurance with Gestational Diabetes is extremely easy to qualify for, and rates are affordable. Simply reach out to us and allow us the opportunity to find you the best life insurance policy possible.

To determine all your options with a history of gestational diabetes, simply fill out a quote request, or contact. We’ll collect some basic health information from you, and share with you what life insurance companies will be the best priced for your health profile.

What are the Best Life Insurance Companies for Diabetics?

Unlike other websites, we’ll first point out that there is NO ONE best company. The best life insurance company is going to depend on your Diabetes history, and your health profile. Until you share certain information with an agent, it’s impossible to determine what company or companies are going to be the best.

Below are some of the life insurance companies we feel that tend to underwrite those with Diabetes Fairly:

Foresters Financial – Great for Non Medical Exam Policies. Depending on your age, you may qualify for up to $400,000 of coverage. Application process usually takes 2-3 days. They also will offer policies that require examinations.

Midland National – Great for individuals with Type 1 and Type 2 Diabetes. Depending on your complete health profile, Midland National can be extremely competitive. Products currently offered include term and permanent types of life insurance.

American National Insurance Company – Great for those looking for ‘living benefit’ riders. American National is extremely competitive to those with Diabetes. Currently, they are offering term, and permanent forms of life insurance.

Royal Neighbors of America – Great for those seeking Burial Insurance or Final Expense Insurance policies. They are extremely favorable to underwriting the Diabetes community. Most people with Diabetes will have no issues qualifying.

John Hancock – Great for those who use Fitbit or Apple Watch to track their activity and exercise data. If willing to share data, and routinely provide your information in an ongoing manor, John Hancock may offer ‘slight’ discounts on premiums. While this ongoing downloading of information is tiresome, for certain people it’s worth the discounts

Gerber Life Insurance – Great for those who have severe health issues, and would only qualify for guaranteed acceptance policies. Many people have sever health issues, that limit them to guaranteed issue policies Symetra– Symetra is an excellent life insurance company that may be the best priced option for many people with Diabetes. They offer both Term, and Permanent forms of life insurance to consumers.

Kansas City Life – KC Life has been in business since 1895. They provide members of the Diabetes community both term and permanent forms of life insurance. For some individuals, KC Life could be the best fit for them.

Diabetes Life Insurance Factors

Life insurance companies will assess how much of a “risk” you are to insure, based on your diabetes conditions and lifestyle. If you are a higher risk, your premiums will be higher. Diabetics are generally considered a high risk, but how much you pay will depend on several factors. Below are the types of information life insurance companies will use, to determine your eligibility for coverage.

How long you’ve been diagnosed – the longer that you’ve been diagnosed, the higher your premiums are likely to be. However, this isn’t true with EVERY carrier, and this is where we come in to help you find the best life insurance company for you. Certain life insurance companies are not necessarily worried about how long you’ve had diabetes, but rather how well your control is of our diabetes..

How well controlled is your diabetes – the better it’s controlled through medications, diet, and exercise, the lower your premiums may be. In most cases, if we can show your A1C and Diabetes history is favorable, your premiums will be better priced compared to someone with an unfavorable A1C. People with diabetes can qualify for healthy lifestyle credits who can show that their A1C is well managed.

How much medication and which medications do you take for your diabetes – medications tend to have negative symptoms in the body, which can make you a higher risk. Various life insurance companies will look at your Diabetes medications differently. Some will ‘rate’ you higher depending on the amount of insulin you are taking. Other companies are not concerned with the amount of insulin you take. In some cases, if you only take oral medication to control your diabetes, you’ll receive ratings comparable to a person who doesn’t have diabetes.

Any diabetes complications – Neuropathy, Retinopathy, Diabetes amputations etc. If your complications are severe, your rates will be higher for life insurance. You may even be declined all together for life insurance due to severe diabetes complications.

Other general health questions – height, weight, family history, tobacco usage, occupations, foreign travel etc.

One of the biggest factors in determining your premiums and coverage is your A1C history. Your A1C will generally give an Underwriter an accurate representation of how well managed your diabetes is. The lower your A1C is, generally lower your rates will be.

This isn’t always the case, as some companies are more concerned about your ENTIRE health history profile.

Meaning that if you live a healthy lifestyle, but for whatever reason you can’t get your A1C below 8.0, you would receive similar rates to a person with Diabetes who has an A1C of 6.0.

Since we specialize in working with the Diabetes community, we will recommend the best life insurance company based off your COMPLETE health profile. We know the various underwriting guides to several A rated life insurance companies. So please use our expertise to your advantage.

With all traditional life insurance policies, you’ll be required to have a medical exam. The medical exam will consist of measuring your blood pressure, height, weight, and a blood and urine sample. The samples will be sent to see if you have any other medical complications.

In addition, life insurance companies will review your Diabetes history, and additional medical records. All of this information will determine your ‘final offers’ and ratings. All the various life insurance companies will view your Diabetes history differently. This is why you want to work with Diabetic life insurance specialists such as us, since we’ll run your profile past multiple life insurance companies.

You may have no medical exam life insurance options available to you. If you don’t wish to complete a paramedical exam, certain people with diabetes can opt for a non medical exam life insurance policy. Companies will still ask you basic health questions, diabetes history questions, prescription drug background check, and will also do a MIB ( medical information bureau) review. All of this information will allow the underwriters to determine if you qualify or not.

Most people are approved for these no medical exam policies in two to three days. If you don’t want to wait weeks for an underwriting decision, a non medical exam policy may be ideal for you.

Frequently Asked Questions

• Can you get life insurance with Diabetes?

Yes!!! You can absolutely qualify for life insurance with diabetes. Life insurance rates for diabetics are at an all time low. It’s honestly never been easier to qualify for coverage, as a person with diabetes. Best way to determine what your options are is to simply contact us, or fill out a quote request.

• Is Life Insurance More Expensive With Diabetes?

Having a chronic illness such as diabetes may cause your premiums to be higher, compared to a person who isn’t diabetic. Many people with type 2 diabetes receive life insurance rates that are Standard or better. Unfortunately, if having type 1 diabetes, you will most likely receive a policy with ‘table’ ratings that are going to make the policy more expensive. Without knowing what a person’s overall health is, it’s impossible to determine what rates, and plans, a diabetic may qualify for.

• Do I Need to Complete a Medical Exam?

Depending on your overall health, and diabetes profile, you may be able to qualify for no medical exam life insurance policies. It’s impossible to determine this, until you speak with an agent, or share with us your health profile.

If needing $500,000 or less, a non medical exam policy may be a good fit for you. For some individuals who need more than $500,000, you could take out multiple policies, to reach the amount of life insurance coverage you need.

Also, certain life insurance companies may be able to provide up to $1 million in coverage by reviewing your medical records. Your recorded health information, once reviewed by an underwriter, would determine your exact rates. This is a great option for those who do not want to take the time, and have a paramed exam completed.

• What Types of Life Insurance Policies can a person with Diabetes Qualify for?

People with any type of diabetes may qualify for term life insurance, whole life insurance or a type of guaranteed universal life insurance coverage. The very same options that people who do not have diabetes qualify for.

• How can a Person with Diabetes Qualify for lower life insurance rates?

One of the best ways to make sure you can qualify for the best life insurance rates, is to work on your control of your Diabetes. Be compliant with your doctors orders, follow a strict diet, and establish a fitness routine. Wen companies look at your health profile, anything we can show them that puts your profile in a ‘favorable’ light will lead to lower premiums.

• How Hard is it to Obtain Life Insurance with Diabetes?

Over time, life insurance companies have evolved. Currently, it’s never been easier to qualify for life insurance, if you have a form of diabetes. The key is to work with people who are trained to work with the diabetes community. Like Diabetes 365 !!!! People with Diabetes have more options for life insurance coverage than at any other point in time.

• What Medical Information is Needed, if I consent to a Blood and Urine test?

When applying for life insurance, companies will not be able to determine your overall health by looking at your application. If you’re capable of providing blood, and urine tests, these lab results will help determine what type of risk you may be. If you have type 1 diabetes, policies that require this testing may be the only option you’d have.

In addition, companies would like to review past medical records. This is simply to see what type of control you have of your diabetes, and to see if there are any complications from this disease. The better your lab results, and medical records look, the better your premiums for life insurance will be.

• What is the application process for Life Insurance?

The application process is probably a lot simpler than you imagine. To start with, after discussing your life insurance needs with your agent, you’ll complete a brief initial application. This application generally takes 15 minutes to complete, and can be done online or over the phone with your agent.

Next, we’ll order the necessary medical records, from your medical professionals. Generally, you will not need to do anything with this as our back office handles this.

While we are waiting for the medical records to be received, we’ll provide to you the local examination’s company contact information. You’ll be able to contact them, and schedule the paramedical exam at a time convenient to you.

Once medical records, and lab results are received, offers can then be made by various life insurance companies. Your agent will present these offers to you, and then you can ultimately decide on how to have the policy issued.

Life Insurance with Type 1 Diabetes

Type 1 diabetes can occur at any time, but in the past has been most often diagnosed at an early age. This is the main reason why Type 1 Diabetes is referred to as “Juvenile Onset Diabetes.” The later onset of diabetes at an older age (teens) has become more prevalent. With type 1 diabetes, the pancreas doesn’t produce insulin. In some cases, you may be diagnosed as a Type 1 Diabetic in your 40’s or 50’s.

The biggest myth in the diabetic community is: type 1 diabetics can’t qualify for life insurance

Affordable life insurance for type 1 diabetics can be obtained, but it is more difficult. People with type 1 diabetes are at a higher risk for heart disease, kidney damage, neuropathy, and other healthy complications. These risks make insurance companies wary of insuring type 1 diabetics. Often times if you are approved, your type 1 diabetes life insurance policy will have extra ‘table ratings’ that lead to higher premiums.

Great news if you have Type 1 diabetes! Life insurance companies are offering rates that are at all time lows. Bad news is, almost 99% of offers will be for what’s referred to as Sub-Standard or Table rated pricing. You will not receive Standard Plus or Preferred offers. Rarely, a person with Type 1 Diabetes will qualify for a Standard rating.

Not all companies will approve people who have Type 1 diabetes. If diagnosed at a young age, certain companies will not even consider for coverage. However, other companies will have no problems approving you for type 1 diabetes life insurance. This is why you need to work with an agency, like Diabetes 365. We can determine what companies may offer coverage, and most importantly, help you find the ones priced the most competitively. Here is an article that discusses some tips on how to secure the best possible life insurance rates with Type 1 Diabetes: Tips for applying for life insurance with Type 1 Diabetes.

Here’s an INSIDER tip: Avoid websites such as Policy Genius, Select Quote, and other sites where agents are NOT trained properly. They show FAKE quotes on their websites, that trick people into applying. The recommendations made at places like these are rarely in the best interest of a consumer. Oftentimes they state that Mutual of Omaha or Prudential are the best options. However, that’s rarely the case.

Those are two good life insurance companies, but there are better priced options 90% of the time. You may qualify for specialized type 1 diabetic life insurance rates, but that’s determined by your complete health profile. Simply reach out to us, and let us see if you qualify.

With type 1 diabetes, an important factor in your life insurance policy will be how well controlled your diabetes is. Your A1C will play a large role in how you’re rated. An A1C around 7 or lower, and no other major health concerns or diabetes complications will get you Sub-Standard offer. This means you would pay a slightly higher premium then an individual without type 1 diabetes.

If your A1C is about 7.0, it’s not the end of the world. It simply means that you’ll pay slightly higher premiums for life insurance. In event your A1C is about 8.5, only a few companies may consider your for life insurance. Don’t worry! We are here to help you find the best priced life insurance coverage with type 1 diabetes. There’s NO need in filling out several applications, and just hoping for the best. Just work with type 1 diabetic life insurance specialists like us! Everybody has a different health profile. That’s why we want to take the time necessary to determine what your best life insurance options are.

If you have other significant health issues, along with not having the best control of your diabetes, traditional life insurance may not be an option. You may have to explore guranteed acceptance life insurance plans, that are designed for higher risk applicants.

If you have type 1 diabetes, you will NOT qualify for standard plus or preferred ratings. Generally, STANDARD ratings are best case scenario, and that rating will be tough to qualify for. Beware of agents only quoting STANDARD rates as they are most likely intentionally misleading you. Also, you most likely will not have as many life insurance companies to choose from, compared to people with type 2.

Over time, the Type 1 Diabetes community has had an easier time finding coverage. Life insurance for Type 1 Diabetics has never been less expensive. If having Type 1 Diabetes, you may even qualify for non-medical exam life insurance policies. To determine if you qualify for a no medical exam life insurance policy with diabetes, simply contact us.

What you will need to do, in order to receive REAL and ACCURATE quotes is to provide an agent your diabetes history, and some other basic health information. Many people with type 1 diabetes get tricked by unethical agents. Those agents provide FAKE quotes, to simply get you to apply with them. Then the actual offers of life insurance come back much, much higher. In our eyes, that’s not a good way of treating a consumer.

The truth is, life insurance with type 1 diabetes is going to be higher in price, compared to people with type 2 diabetes. However, people with type 1 diabetes can do a few things, to lower their life insurance premiums.

See an Endocrinologist – Seeing an endocrinologist regularly leads to better control of your diabetes. Life insurance companies love to see a person with type 1 diabetes working with a diabetes specialist.

Use Technology – Some life insurance carriers may offer lower rates if you are using CGM devices, FitBit’s, or even an insulin pump.

Have a Regular Exercise Routine – Showing companies that you exercise regularly, may lead to discounted rates for certain life insurance companies.

Complete a Paramedical Exam – In most cases, to achieve the lowest life insurance rates with type 1 diabetes, you’ll need to complete a paramedical exam. This is simply a blood and urine exam. In addition to your lab results, companies will also want to review your most recent diabetes medical records. Allowing an insurance carrier to review your complete health profile tends to allow them to make the best possible offer.

If you are overwhelmed at the thought of looking for diabetic life insurance, there are experienced insurance specialists such as us, to help you. Don’t feel overwhelmed! We are here to help! Simply contact us, have a brief five minute conversation, and our agents will be able to point you in the right direction!

Type 2 Diabetes Life Insurance

Type 2 diabetes, normally occurs in adults after the age of 40, but can be diagnosed earlier. With type 2 diabetes, the pancreas still produces insulin, but doesn’t produce enough.

Over 30 million people are diagnosed with type 2 diabetes in the United States. Type 2 represents around 90 – 95% of the diabetic community. Good news–some insurance companies have started specializing in insuring type 2 diabetics, because of its increasing population.

For certain individuals, you may be able to qualify for special life insurance rates. These Type 2 diabetic life insurance rates could be up to 20% lower, than rates available to others. NOT everyone will qualify, as this product is geared toward those people with Type 2 diabetes who live a healthy and active life style. Contact us to see if you qualify for these discounted rates.

What medications are taking for your Type 2 Diabetes?

Do you use tobacco?

What is your A1C?

Any Diabetes Complications?

Any other significant health issues?

Do you watch your Diet?

What is your occupation?

How often do you go to the doctor?

You will be asked how you control your diabetes. Is your diabetes controlled mostly with your diet and exercise or a combination of medications? The types and frequency of your medications may affect your premium and coverage. Various type 2 life insurance companies have different underwriting guidelines. Don’t let this confuse you, as we’ll tell you which companies would work best for your personal situation

Type 2 Diabetes Life Insurance Without Taking Diabetes Medications

Many people who are diagnosed with Type 2 diabetes, will be able to control their condition without taking any form of diabetes medications. Maintaining a healthy lifestyle, watching your diet, and exercising regularly may allow you to control your type 2 diabetes. If you fall into this category, obtaining life insurance with Type 2 diabetes will be a breeze.

If this is the case, you would most likely be viewed as a favorable candidate for life insurance coverage. Many people with type 2 diabetes, can obtain Standard, to Preferred life insurance rates. To qualify for the best premiums possible, companies will require you to complete a blood/urine test, as well as possibly reviewing your most recent diabetes medical records. Here are some sample quotes:

$250,000 Level Term Life Insurance – Female Non-Tobacco User

40 Year Old

50 Year Old

60 Year Old

10 Year Term

$17-30 monthly

$32-50 monthly

$64-80 monthly

15 Year Term

$20-40 monthly

$40-58 monthly

$83-102 monthly

20 Year Term

$24-45 monthly

$48-67 monthly

$115-132 monthly

25 Year Term

$32-50 monthly

$66-85 monthly

$194-215 monthly

30 Year Term

$37-60 monthly

$77-100 monthly

N/A

$250,000 Level Term Life Insurance – Male Non-Tobacco User

40 Year Old

50 Year Old

60 Year Old

10 Year Term

$20-36 monthly

$39-60 monthly

$87-105 monthly

15 Year Term

$22-40 monthly

$48-70 monthly

$119-140 monthly

20 Year Term

$29-50 monthly

$64-85 monthly

$164-185 monthly

25 Year Term

$49-56 monthly

$92-110 monthly

$267-300 monthly

30 Year Term

$45-70 monthly

$108-130 monthly

N/A

Also, you’d have several options for non medical exam policies. Many companies would be able to approve you in a matter of days. Life insurance rates would be slightly higher. To see what options you’d qualify for, simply reach out to us, and speak with an agent.

Type 2 Diabetes Life Insurance Taking Oral or Insulin Medication

In a perfect world, life insurance companies would prefer you to control your Type 2 Diabetes with your diet and exercise regimen. However, this isn’t always the case. Life insurance with type 2 diabetes is still usually pretty easy to obtain.

Certain life insurance companies will reward Type 2 Diabetics with better rates, if your Diabetes is controlled using this method. On the other hand, other life insurance companies will not rate you higher if you’re Type 2 Diabetes is controlled with Oral medication, insulin, or maybe a combination of the two. Many companies understand that you can maintain a healthy lifestyle, while having type 2 diabetes.

When working with Diabetes365, we’ll let you know which life insurance companies won’t rate you higher for the use of diabetes medications. We’ll make sure to recommend the companies that will underwrite your health profile the most competitively. At the end of the day, companies want to make sure that your type 2 diabetes is well controlled. If that requires medication, then so be it.

Life insurance companies typically prefer people to be diagnosed age 45 or later. However, depending on a person’s lifestyle, being diagnosed at a younger age may not increase your premiums. If we’re able to show underwriters that you live a healthy lifestyle, and are exhibiting excellent control of your type 2 diabetes, you’ll have no issues receiving policies with rates comparable to people without diabetes.

Examples

An example of an applicant who would receive “preferred” rates:

Diagnosed with type 2 after age 50

Manages diabetes with a healthy diet and exercise

Is in a healthy BMI range

Fasting blood sugars under/near 100

A1C 7.5 or below

No Diabetes complications

In contrast, an example of an applicant with “standard” rates:

Diagnosed with type 2 at age 30

Doesn’t eat well or exercise often

Considered “overweight”

Fasting blood sugar is 125

A1C is above 8

No Diabetes complications

Based off these two Diabetes health profiles, there could be a difference of $1,000 to $2,000 per year in premiums. Wanting the lowest rates possible? Simply reach out to us, and let us review your health profile. Here are some sample quotes for life insurance for people with type 2 diabetes, controlling their condition with medications:

$250,000 Level Term Life Insurance – Female Non-Tobacco User

40 Year Old

50 Year Old

60 Year Old

10 Year Term

$17-50 monthly

$32-75 monthly

$64-100 monthly

15 Year Term

$20-56 monthly

$40-89 monthly

$83-125 monthly

20 Year Term

$24-70 monthly

$48-67 monthly

$115-160 monthly

25 Year Term

$32-75 monthly

$66-105 monthly

$194-250 monthly

30 Year Term

$37-90 monthly

$77-125 monthly

N/A

$250,000 Level Term Life Insurance – Male Non-Tobacco User

40 Year Old

50 Year Old

60 Year Old

10 Year Term

$20-54 monthly

$39-86 monthly

$87-130 monthly

15 Year Term

$22-62 monthly

$48-95 monthly

$119-165 monthly

20 Year Term

$29-70 monthly

$64-110 monthly

$164-205 monthly

25 Year Term

$49-75 monthly

$92-135 monthly

$267-330 monthly

30 Year Term

$45-95 monthly

$108-180 monthly

N/A

Generally speaking , Type 2 Diabetes life insurance will be less expensive, compared to a person with Type 1 Diabetes. To begin getting an idea to what Term Life Insurance, or Whole Life Insurance options you’d have, simply contact us. Our agents are happy to work with you, and make the best possible recommendations for you and your family. The biggest mistake people with diabetes tend to make is not speaking with agents who specialize, in the diabetes life insurance market place.

Life Insurance with Pre-Diabetes

Many people may have pre-diabetes, and possibly not even know they fall into this category. It’s reported according to Centers for Diabetes Control and Prevention, that nearly 84 million people could be living with Pre-Diabetes. Life insurance with Pre-Diabetes couldn’t be easier.

Depending on where your current A1C level is, and what your overall health picture looks like, you’ll most likely be in the STANDARD to Preferred Plus rating range. You’ll also have plenty of no medical exam life insurance options to choose from as well.

Life Insurance with Gestational Diabetes

Having a history of Gestational Diabetes shouldn’t stop you from finding affordable life insurance coverage. Most of our clients tend to qualify for Standard to Preferred ratings. These are the types of rates that people without Diabetes qualify for.

No Exam Life Insurance for Diabetics

No exam life insurance for diabetics policies are exactly what they sound like. With these policies you can get coverage without having to take a medical exam.

Depending on your overall health profile, these may be the best priced policies, for you.

No exam policies are great for several situations:

You have a high A1C

You aren’t controlling your diabetes

You are a tobacco user

Considered overweight

You want life insurance quickly

Most no exam life insurance policies can be completed in 24 to 72 hours. While no exam life insurance is a great way to get insurance quickly, the convenience comes with a large price tag. Most no exam policies can cost you 25% to 50% more than a policy that requires a medical exam.

Another disadvantage is the coverage limit. Each company will have a different limit, but depending on your situation, the coverage might not be enough. Oftentimes, life insurance companies will limit people with Diabetes, to $500,000 of coverage without undergoing an exam. Good news though! If needing more than $500,000, you could always take out multiple policies, to address your financial objectives.

Getting Diabetic life insurance without a medical exam, could be the best possible solution for you. To determine what’s best, please speak with us, and our Diabetic life insurance specialists will provide you with unbiased recommendations. Generally, you’d have Term Life Insurance, or Permanent Life Insurance options to choose from. Again, depending on your Diabetes history, we can help make suitable recommendations, and provide you with the various non-medical exam life insurance options.

No medical exam life insurance with diabetes is a pretty straight forward product. You’d provide answers to basic medical questions, and share with your agent a list of medications you are taking. A prescription background check, as well as a Medical Information Bureau review, would also be done by the life insurance company. The information collected, and answers to health questions determines your eligibility.

For some people who do not have the best control of the A1C, a no medical exam policy could be their only choice. Some no medical exam carriers don’t even ask about your A1C reading. This could be advantageous for certain people with diabetes. It’s generally a good idea to speak with an agent, share your situation with them, and let them guide you to the product that best suits you.

Burial Insurance with Diabetics

For certain individuals, perhaps you only need a smaller amount of life insurance, to address final expenses. If you feel the need to have life insurance to protect your family, and to pay for burial costs, funeral expenses, a burial insurance policy might be suitable. Burial insurance for diabetics can easily be obtained. It’s simply a matter of working with agents who are specialize in assisting those with diabetes obtain a policy.

Burial insurance for diabetics can easily be obtained. It’s simply a matter of working with agents who are specialize in assisting those with diabetes obtain a policy.

A burial insurance policy is simply a ‘smaller’ amount of whole life insurance, designed to cover all the final expenses that come at the end of one life. These policies have the following features:

No Medical Exam’s

Premiums that never increase

Life insurance coverage that never expires

Death benefit that’s paid to beneficiary in a tax free and lump sum manner

Most people with Diabetes will not have issues finding coverage. To determine what rates and options you’d have available, simply reach out to us. An agent can guide you in the right direction.

Summary

Regardless of which type of diabetes you have, the bottom line is: you can have affordable life insurance with Diabetes. A person with diabetes will most likely pay a higher monthly premium for life insurance than a non-diabetic, but that doesn’t mean your premium has to be outrageous. Finding the right agent can make a significant difference in the coverage and premium.

Here at Diabetes 365, we will advocate on your behalf, and help you find the best priced life insurance policy. You’ll only receive honest information from us. We do not provide fake, or low ball quotes, like other agents do.

It doesn’t matter if you have Gestational Diabetes, Type 1 Diabetes, or even Type 2 Diabetes, we can help. Maybe you don’t know how much life insurance you need. Maybe you don’t know what type of life insurance policy your family needs. We can help with all these questions. Contact us today, and let a friendly agent help you and your family out. We will make the diabetes life insurance application process a breeze for you.

Get Life Insurance Quotes Now

Matt Schmidt

Matt Schmidt is a nationally licensed diabetes insurance expert. Over this time frame he's helped out over 10,000 clients secure life insurance coverage with Diabetes. He's frequently authors content to Forbes, Entrepreneur, The Simple Dollar, GoBanking Rates, MSN, Insurancenews.net, and Yahoo Finance and many more.

Matt Schmidt is also the Co-Founder of Diabetes Life Solutions and Licensed Insurance agent. He’s been working with the Diabetes community for over 18 years to find consumers the best life insurance policies. Since 2011, he has been a qualified non-member of MDRT, the most prestigious life insurance trade organization in the USA

This mode enables people with epilepsy to use the website safely by eliminating the risk of seizures that result from flashing or blinking animations and risky color combinations.

Visually Impaired Mode

Improves website's visuals

This mode adjusts the website for the convenience of users with visual impairments such as Degrading Eyesight, Tunnel Vision, Cataract, Glaucoma, and others.

Cognitive Disability Mode

Helps to focus on specific content

This mode provides different assistive options to help users with cognitive impairments such as Dyslexia, Autism, CVA, and others, to focus on the essential elements of the website more easily.

ADHD Friendly Mode

Reduces distractions and improve focus

This mode helps users with ADHD and Neurodevelopmental disorders to read, browse, and focus on the main website elements more easily while significantly reducing distractions.

Blindness Mode

Allows using the site with your screen-reader

This mode configures the website to be compatible with screen-readers such as JAWS, NVDA, VoiceOver, and TalkBack. A screen-reader is software for blind users that is installed on a computer and smartphone, and websites must be compatible with it.

Readable Experience

Content Scaling

Default

Text Magnifier

Readable Font

Dyslexia Friendly

Highlight Titles

Highlight Links

Font Sizing

Default

Line Height

Default

Letter Spacing

Default

Left Aligned

Center Aligned

Right Aligned

Visually Pleasing Experience

Dark Contrast

Light Contrast

Monochrome

High Contrast

High Saturation

Low Saturation

Adjust Text Colors

Adjust Title Colors

Adjust Background Colors

Easy Orientation

Mute Sounds

Hide Images

Virtual Keyboard

Reading Guide

Stop Animations

Reading Mask

Highlight Hover

Highlight Focus

Big Dark Cursor

Big Light Cursor

Navigation Keys

Diabetes365 Your Resource for Life

Accessibility Statement

www.diabetes365.org

July 4, 2026

Compliance status

We firmly believe that the internet should be available and accessible to anyone, and are committed to providing a website that is accessible to the widest possible audience,

regardless of circumstance and ability.

To fulfill this, we aim to adhere as strictly as possible to the World Wide Web Consortium’s (W3C) Web Content Accessibility Guidelines 2.1 (WCAG 2.1) at the AA level.

These guidelines explain how to make web content accessible to people with a wide array of disabilities. Complying with those guidelines helps us ensure that the website is accessible

to all people: blind people, people with motor impairments, visual impairment, cognitive disabilities, and more.

This website utilizes various technologies that are meant to make it as accessible as possible at all times. We utilize an accessibility interface that allows persons with specific

disabilities to adjust the website’s UI (user interface) and design it to their personal needs.

Additionally, the website utilizes an AI-based application that runs in the background and optimizes its accessibility level constantly. This application remediates the website’s HTML,

adapts Its functionality and behavior for screen-readers used by the blind users, and for keyboard functions used by individuals with motor impairments.

If you’ve found a malfunction or have ideas for improvement, we’ll be happy to hear from you. You can reach out to the website’s operators by using the following email

Screen-reader and keyboard navigation

Our website implements the ARIA attributes (Accessible Rich Internet Applications) technique, alongside various different behavioral changes, to ensure blind users visiting with

screen-readers are able to read, comprehend, and enjoy the website’s functions. As soon as a user with a screen-reader enters your site, they immediately receive

a prompt to enter the Screen-Reader Profile so they can browse and operate your site effectively. Here’s how our website covers some of the most important screen-reader requirements,

alongside console screenshots of code examples:

Screen-reader optimization: we run a background process that learns the website’s components from top to bottom, to ensure ongoing compliance even when updating the website.

In this process, we provide screen-readers with meaningful data using the ARIA set of attributes. For example, we provide accurate form labels;

descriptions for actionable icons (social media icons, search icons, cart icons, etc.); validation guidance for form inputs; element roles such as buttons, menus, modal dialogues (popups),

and others. Additionally, the background process scans all of the website’s images and provides an accurate and meaningful image-object-recognition-based description as an ALT (alternate text) tag

for images that are not described. It will also extract texts that are embedded within the image, using an OCR (optical character recognition) technology.

To turn on screen-reader adjustments at any time, users need only to press the Alt+1 keyboard combination. Screen-reader users also get automatic announcements to turn the Screen-reader mode on

as soon as they enter the website.

These adjustments are compatible with all popular screen readers, including JAWS and NVDA.

Keyboard navigation optimization: The background process also adjusts the website’s HTML, and adds various behaviors using JavaScript code to make the website operable by the keyboard. This includes the ability to navigate the website using the Tab and Shift+Tab keys, operate dropdowns with the arrow keys, close them with Esc, trigger buttons and links using the Enter key, navigate between radio and checkbox elements using the arrow keys, and fill them in with the Spacebar or Enter key.Additionally, keyboard users will find quick-navigation and content-skip menus, available at any time by clicking Alt+1, or as the first elements of the site while navigating with the keyboard. The background process also handles triggered popups by moving the keyboard focus towards them as soon as they appear, and not allow the focus drift outside of it.

Users can also use shortcuts such as “M” (menus), “H” (headings), “F” (forms), “B” (buttons), and “G” (graphics) to jump to specific elements.

Disability profiles supported in our website

Epilepsy Safe Mode: this profile enables people with epilepsy to use the website safely by eliminating the risk of seizures that result from flashing or blinking animations and risky color combinations.

Visually Impaired Mode: this mode adjusts the website for the convenience of users with visual impairments such as Degrading Eyesight, Tunnel Vision, Cataract, Glaucoma, and others.

Cognitive Disability Mode: this mode provides different assistive options to help users with cognitive impairments such as Dyslexia, Autism, CVA, and others, to focus on the essential elements of the website more easily.

ADHD Friendly Mode: this mode helps users with ADHD and Neurodevelopmental disorders to read, browse, and focus on the main website elements more easily while significantly reducing distractions.

Blindness Mode: this mode configures the website to be compatible with screen-readers such as JAWS, NVDA, VoiceOver, and TalkBack. A screen-reader is software for blind users that is installed on a computer and smartphone, and websites must be compatible with it.

Keyboard Navigation Profile (Motor-Impaired): this profile enables motor-impaired persons to operate the website using the keyboard Tab, Shift+Tab, and the Enter keys. Users can also use shortcuts such as “M” (menus), “H” (headings), “F” (forms), “B” (buttons), and “G” (graphics) to jump to specific elements.

Additional UI, design, and readability adjustments

Font adjustments – users, can increase and decrease its size, change its family (type), adjust the spacing, alignment, line height, and more.

Color adjustments – users can select various color contrast profiles such as light, dark, inverted, and monochrome. Additionally, users can swap color schemes of titles, texts, and backgrounds, with over 7 different coloring options.

Animations – epileptic users can stop all running animations with the click of a button. Animations controlled by the interface include videos, GIFs, and CSS flashing transitions.

Content highlighting – users can choose to emphasize important elements such as links and titles. They can also choose to highlight focused or hovered elements only.

Audio muting – users with hearing devices may experience headaches or other issues due to automatic audio playing. This option lets users mute the entire website instantly.

Cognitive disorders – we utilize a search engine that is linked to Wikipedia and Wiktionary, allowing people with cognitive disorders to decipher meanings of phrases, initials, slang, and others.

Additional functions – we provide users the option to change cursor color and size, use a printing mode, enable a virtual keyboard, and many other functions.

Browser and assistive technology compatibility

We aim to support the widest array of browsers and assistive technologies as possible, so our users can choose the best fitting tools for them, with as few limitations as possible. Therefore, we have worked very hard to be able to support all major systems that comprise over 95% of the user market share including Google Chrome, Mozilla Firefox, Apple Safari, Opera and Microsoft Edge, JAWS and NVDA (screen readers), both for Windows and for MAC users.

Notes, comments, and feedback

Despite our very best efforts to allow anybody to adjust the website to their needs, there may still be pages or sections that are not fully accessible, are in the process of becoming accessible, or are lacking an adequate technological solution to make them accessible. Still, we are continually improving our accessibility, adding, updating and improving its options and features, and developing and adopting new technologies. All this is meant to reach the optimal level of accessibility, following technological advancements. For any assistance, please reach out to